As an Amazon Associate, I earn from qualifying purchases.

Retirement planning is often compared to a complex puzzle, and for many homeowners, the biggest piece of that puzzle is the mortgage. As you approach your golden years, a fundamental question arises: Should you pay off your mortgage early, or are you better off investing that extra cash in the market?

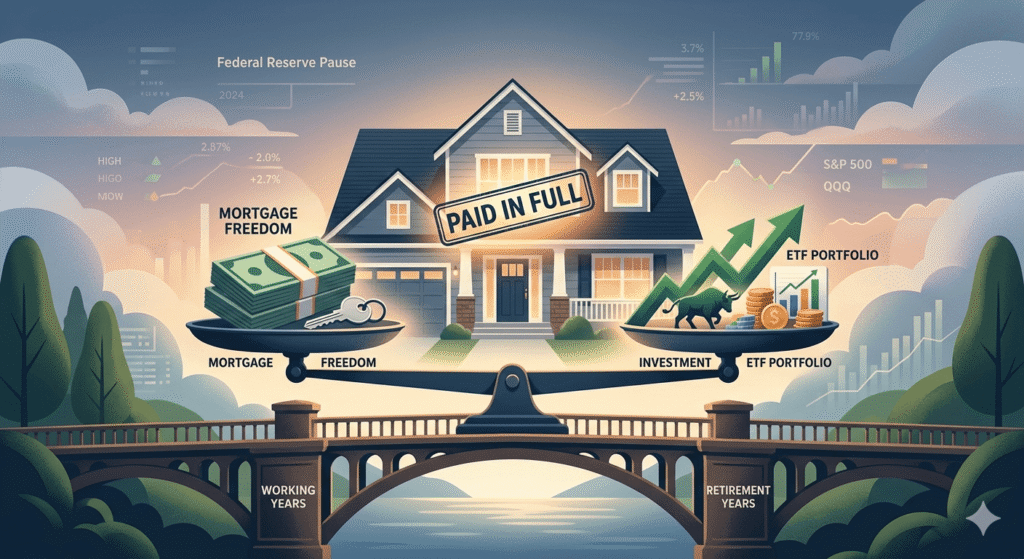

With the current economic landscape featuring a “Federal Reserve Pause” and interest rates hovering around 6%, the answer isn’t as simple as it was a few years ago. This guide explores the mathematical, psychological, and strategic factors to help you make the smartest move for your retirement.

The Math: Interest Rates vs. Market Returns

The most objective way to view this dilemma is through the lens of opportunity cost. Every dollar you use to pay down your mortgage principal is a dollar that isn’t being invested in assets like the S&P 500 or diversified ETFs.

- The Guaranteed Return: Paying off a mortgage with a 6.4% interest rate is functionally equivalent to earning a guaranteed, tax-free 6.4% return on your money. In a volatile market, a guaranteed return of over 6% is highly attractive.

- The Market Potential: Historically, the US stock market has delivered average annual returns of about 7% to 10% over long periods. However, these returns are never guaranteed. If your mortgage rate is locked in at a historic low of 2.5% or 3%, the “spread” between your mortgage cost and potential investment gains is wide, making investing the clear mathematical winner.

- The Spread Analysis:

- Low Mortgage Rate (under 4%): Generally, it is better to keep the mortgage and invest in a diversified portfolio (like SPLG or QQQM).

- High Mortgage Rate (above 6%): The argument for paying off the debt becomes much stronger as the “guaranteed return” nears the “expected market return.”

Cash Flow: The Lifeblood of Retirement

In retirement, your priority shifts from wealth accumulation to cash flow management.

When you no longer have a steady paycheck, your monthly expenses determine how much you must withdraw from your Roth IRA or 401(k). The mortgage is typically a household’s largest monthly expense. By eliminating it, you significantly lower your “burn rate.”

Why a lower burn rate matters:

- Sequence of Returns Risk: If the stock market crashes right after you retire, having no mortgage means you don’t have to sell as many shares at a loss to pay the bank.

- Tax Efficiency: Lower expenses mean you might need smaller distributions from taxable retirement accounts, potentially keeping you in a lower tax bracket.

The Liquidity Trap: Don’t Be “House Rich, Cash Poor”

One of the biggest risks of aggressive mortgage payoff is illiquidity. Home equity is “trapped” wealth. You cannot easily buy groceries with the bricks and mortar of your chimney.

Before putting every extra cent toward your house, ensure you have:

- A Robust Emergency Fund: At least 6 to 12 months of expenses in a high-yield savings account.

- Liquid Investments: Ensure you have enough in accessible accounts to cover unexpected medical bills or home repairs without needing to take out a new loan at current high rates.

Tax Implications in the Modern Era

Historically, the Mortgage Interest Deduction was a major reason to keep a loan. However, since the standard deduction was significantly increased, fewer taxpayers “itemize” their deductions. If you are taking the standard deduction, the tax benefit of your mortgage interest disappears. Always consult with a tax professional to see if your mortgage still provides a meaningful tax shield.

The Psychological Factor: Peace of Mind

We aren’t just robots calculating spreadsheets. For many, the feeling of owning their home “free and clear” provides a level of psychological security that no brokerage account balance can match.

If debt causes you stress or keeps you up at night, the “mental dividend” of paying it off may outweigh the 1% or 2% mathematical advantage of staying in the market. Retirement is about enjoying the fruits of your labor; if a mortgage feels like a burden, shedding it is a valid lifestyle choice.

Strategic Alternatives: The Middle Ground

You don’t have to choose “all or nothing.” Consider these hybrid strategies:

- The Hybrid Approach: Split your extra cash. Put 50% toward the mortgage principal and 50% into your brokerage account.

- The “Lump Sum” Strategy: Keep your money invested in a dedicated “Mortgage Payoff Fund” (using conservative ETFs or Bonds). Once that fund grows large enough to cover the remaining balance, you can decide whether to write the check or keep the money growing.

- Targeting the Interest Rate: If you have a high-interest mortgage, consider refinancing when rates eventually drop below your current mark, rather than rushing to pay it off now.

The Final Verdict

Is paying off the mortgage the first thing you should do? Usually, no.

Before attacking the mortgage, ensure you have:

- Eliminated high-interest consumer debt (credit cards).

- Maximized your employer’s 401(k) match.

- Built an emergency fund.

- Calculated your projected retirement income.

Once those pillars are in place, paying off your mortgage becomes a powerful tool to de-risk your retirement. If your interest rate is high and your goal is maximum security, paying it off is a “Smart Path to Retirement”.

What do you think? Are you prioritizing a debt-free home, or are you betting on the resilience of the US stock market? Let us know in the comments below!

“Paying off your mortgage is a powerful tool to de-risk your retirement. To help you build a stronger investment philosophy as you plan your ‘Smart Path to Retirement,’ consider adding [The Psychology of Money] to your reading list. It’s one of the few books that changed how I view my own portfolio.”

Disclaimer: I am not a financial advisor. This post reflects my personal investment philosophy and strategy. All investments carry risk, and past performance is not indicative of future results. Please conduct your own research before making financial decisions.