As an Amazon Associate, I earn from qualifying purchases.

Retirement planning is often discussed in abstract terms—people talk about “saving money” or “investing for the future.” But as a business owner, I view things differently. Retirement isn’t a vague aspiration; it is a long-term financial project. If we define the destination as $750,000 and the timeline as 17 years, the goal ceases to be a dream and becomes a mathematical equation.

To succeed in this project, one must stop acting like a spectator and start acting like a CEO. You need a strategy, a portfolio structure, and, most importantly, the discipline to execute regardless of market volatility.

1. The Mathematics of Your Retirement Goal

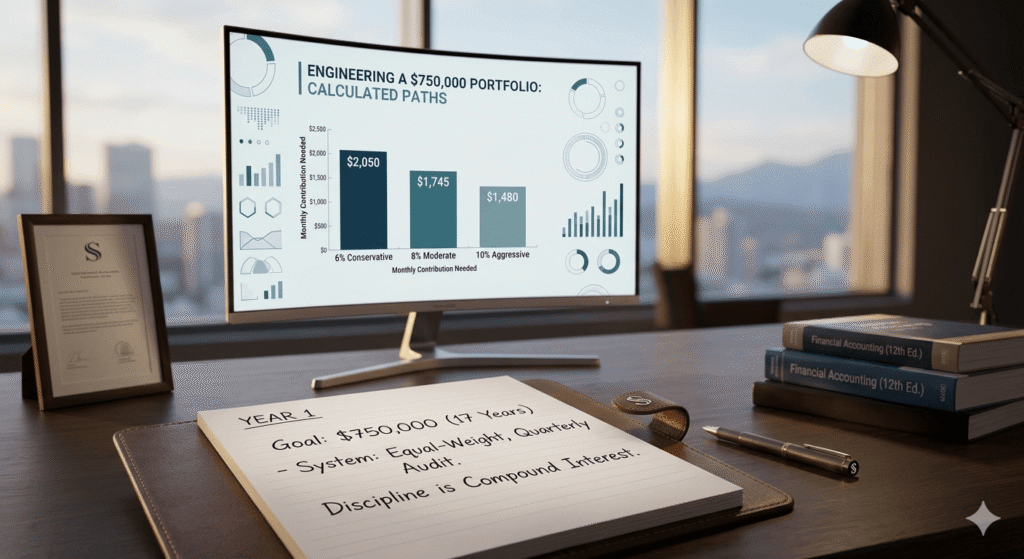

The most common mistake amateur investors make is failing to account for the power of compounding combined with consistent contributions. To reach $750,000 in 17 years, you must understand the relationship between your monthly contribution and your expected annual rate of return.

Even a small difference in your annual return can significantly alter the amount you need to save every month. Let’s look at the numbers:

| Expected Annual Return | Monthly Contribution Needed | Total Principal Invested |

|---|---|---|

| 6% (Conservative) | $2,050 | $418,200 |

| 8% (Moderate) | $1,745 | $355,980 |

| 10% (Aggressive) | $1,480 | $301,920 |

Export to Sheets

Note: These figures assume monthly contributions with interest compounded monthly. They do not account for taxes, inflation, or fees.

The takeaway is simple: If you rely on a conservative approach, you must compensate with a higher savings rate. However, if you are willing to embrace a diversified growth-oriented portfolio, you allow the market to do more of the “heavy lifting” for you.

2. Anatomy of a Balanced Portfolio

My personal investment strategy is built on a “Core-Satellite” philosophy, managed with an equal-weight discipline. By spreading capital across market leaders, dividend-growers, and defensive assets, I minimize the impact of any single sector failing.

My portfolio is currently composed of the following assets, held at equal weights:

- The Market Core (QQQM, SCHD, SPLG): This is the foundation. QQQM provides exposure to the innovation-heavy Nasdaq-100, SPLG offers low-cost access to the S&P 500, and SCHD focuses on dividend growth. Together, they balance market beta with steady income.

- The Growth Satellites (GOOGL, AMZN, NVDA, PLTR): These companies are the engines of the future. AI, cloud computing, and big data are structural shifts in the global economy. By allocating to these leaders, we participate in the transformative growth of the 21st century.

- The Defensive Stabilizers (BND, WMT): Every business needs a balance sheet cushion. BND provides interest-rate sensitive stability, while WMT acts as a counter-cyclical anchor. When the economy faces headwinds, these assets help reduce the overall portfolio drawdown.

3. The Business Owner’s Mindset: Systematic Investing

Why do I choose to manage this portfolio with equal weights? It forces a disciplined habit that most investors lack: Mechanical Rebalancing.

In a standard portfolio, winners run wild, and losers drag you down. In an equal-weight portfolio, you are forced to rebalance periodically. When GOOGL or NVDA has a stellar year, their weight in your portfolio increases. To bring them back to “equal weight,” you must sell a portion of that gain and redistribute the capital into the assets that have lagged.

This is the ultimate expression of the “Buy Low, Sell High” strategy. You aren’t guessing the market; you are systematically maintaining your risk profile.

Furthermore, you must automate the process. On the day your income hits your bank account, a portion should be redirected to your brokerage. By automating this, you remove the emotional decision-making process. You aren’t “choosing” to invest; you are executing a business process.

4. Overcoming Market Noise

One of the greatest challenges to a 17-year plan is the “news cycle.” Headlines about wars, inflation, or political instability are designed to create fear. When you manage your portfolio like a business, you learn to treat these headlines as mere noise.

When the market dips, a business owner doesn’t sell the company; they look for ways to optimize operations. When your portfolio dips, don’t look for the “sell” button. Look at your equal-weight targets. Ask yourself: “Am I buying these high-quality assets at a discount?” If you have automated your contributions, market corrections simply mean you are buying more shares for the same amount of money.

5. Conclusion: Consistency is the Real Compound Interest

Reaching $750,000 in 17 years is entirely achievable, but it requires more than just picking the right stocks. It requires the consistency of a business owner.

Your portfolio is not a lottery ticket. It is a long-term compound interest machine. By funding it regularly, maintaining a disciplined asset allocation, and keeping your eyes fixed on the 17-year horizon, you will outpace the short-term fluctuations that derail less disciplined investors.

Start today. Calculate your monthly contribution, automate your transfer, and stay the course. Your future self is depending on the discipline you cultivate right now.

Disclaimer

The information provided on Smart Path to Retire is for educational and informational purposes only and does not constitute professional financial, investment, or legal advice.

As a business owner sharing my personal journey toward retirement, the strategies and asset allocations discussed here reflect my own opinions, risk tolerance, and research. They are not intended to be—and should not be interpreted as—financial advice or a recommendation to buy or sell any specific securities (including QQQM, SCHD, SPLG, GOOGL, AMZN, NVDA, PLTR, BND, or WMT).

- Investment Risk: All investing involves risk, including the possible loss of principal. Markets are volatile, and past performance is never a guarantee of future results.

- Do Your Own Research (DYOR): Every individual’s financial situation, goals, and risk tolerance are different. You should conduct your own due diligence and consult with a qualified financial advisor, tax professional, or accountant before making any investment decisions.

- No Guarantees: Any mention of specific returns, financial goals, or growth projections is purely illustrative and based on historical data or personal planning. No specific financial outcome is guaranteed.

By using this website, you acknowledge that you are responsible for your own financial decisions. The author of Smart Path to Retire shall not be held liable for any losses or damages resulting from the use of, or reliance on, the information provided on this site.