As an Amazon Associate, I earn from qualifying purchases.

The financial landscape of 2026 has been nothing short of extraordinary. With the semiconductor sector reaching new heights and the S&P 500 defying gravity, investors find themselves at a crossroads. Is this the beginning of a multi-decade productivity boom, or are we witnessing the final, frantic sparks of a historic bubble?

To navigate this uncertainty, we must look at the two prevailing philosophies currently dominating Wall Street. On one side, we have the legendary macro trader Paul Tudor Jones, who preaches caution and historical perspective. On the other, we have Tom Lee, the Head of Research at Fundstrat, whose unwavering optimism has correctly anticipated much of the recent rally.

Paul Tudor Jones: The 1999 Warning

In a recent, widely discussed interview on CNBC’s “Squawk Box” (May 2026), Paul Tudor Jones delivered a sobering assessment of the current market. Jones, known for predicting the 1987 crash, sees striking parallels between today’s price action and the late 1990s.

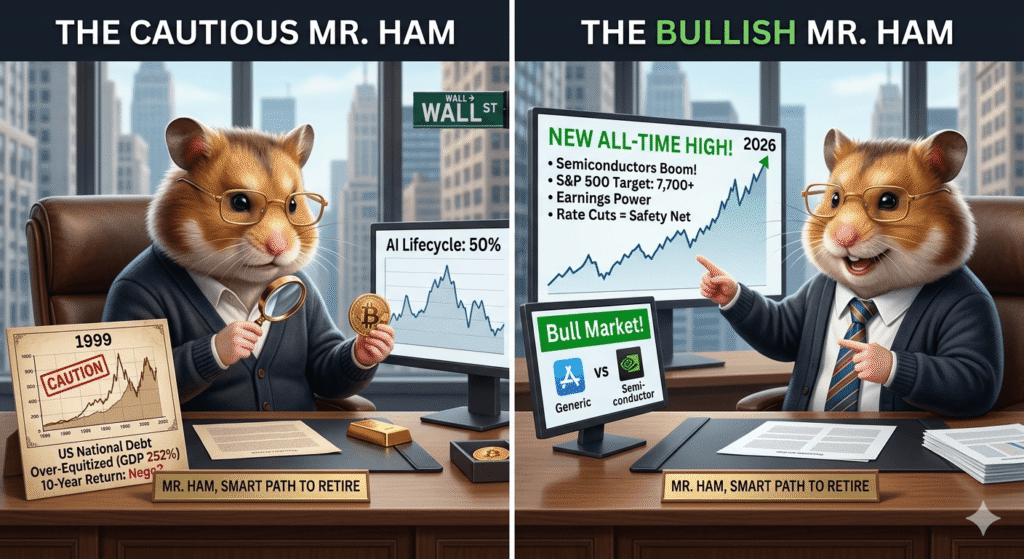

The 1999 Deja Vu

Jones argues that we are currently in a phase that mirrors 1999, roughly one year before the peak of the Dot-com bubble. While he acknowledges that the market still has momentum, he suggests we are in the “final innings” of this particular cycle. According to his analysis, the AI productivity cycle is about 50% to 60% complete, potentially leaving about 1 to 2 years of upside before a significant correction occurs.

The Danger of “Over-Equitization”

A core pillar of the Jones thesis is the sheer scale of the US market relative to the economy. He points out that the US stock market capitalization is roughly 252% of GDP. This level of “over-equitization” means that the economy is no longer just reflected by the market; it is increasingly dependent on it. If a correction happens, the impact on tax revenue and consumer spending could lead to what he describes as a “breathtaking” adjustment.

Strategic Hedging with Bitcoin

Given his concerns about the US national debt and the potential for long-term inflation, Jones remains a staunch advocate for “limited supply” assets. In his May 2026 commentary, he reiterated that Bitcoin remains a superior hedge compared to gold because its supply is mathematically capped, making it a critical insurance policy for a modern portfolio.

Tom Lee: The Case for a Structural Bull Market

Contrast this with the view from Tom Lee and the team at Fundstrat. In recent investor notes and media appearances, Lee has dismissed the 1999 comparison, arguing that the fundamental drivers of today’s market are vastly different from the speculative frenzy of twenty-five years ago.

Earnings Power vs. Speculation

Lee’s primary counter-argument is based on earnings quality. In 1999, many high-flying tech companies had no revenue and even less profit. Today, the leaders of the AI revolution—companies like NVIDIA, Microsoft, and the major semiconductor players—are generating massive free cash flow and historic profit margins. From Lee’s perspective, these companies are not “bubbles”; they are the most efficient profit machines in history.

The Federal Reserve’s “Safety Net”

Another critical difference Lee highlights is the stance of the Federal Reserve. While the Fed was tightening into the 1999 bubble, the 2026 environment is defined by a transition toward lower interest rates. This shift provides a valuation floor and ensures that liquidity remains available to support asset prices, making a catastrophic “Dot-com style” crash less likely in the near term.

A Target of 7,700 and Beyond

While others fear a peak, Lee has been raising his price targets for the S&P 500, suggesting that the index could reach 7,700 or higher. He views the current “Bull Market” in semiconductors as a reflection of a generational shift in global productivity that will take years, not months, to fully play out.

Comparing the Two Titans

| Feature | Paul Tudor Jones (CNBC Interview) | Tom Lee (Fundstrat Reports) |

|---|---|---|

| Current Market Phase | Late-stage bubble (1999 analog) | Structural, earnings-driven expansion |

| Primary Concern | US Debt and Over-valuation | Missing the rally due to fear |

| AI Outlook | 1-2 years of growth remaining | Multi-year productivity revolution |

| Key Recommendation | Bitcoin, Gold, and Diversification | Aggressive positioning in Tech & Semis |

Export to Sheets

Investor Takeaway: Finding the Middle Ground

As a small business owner or a retirement planner, how do you reconcile these two brilliant yet opposing views?

- Respect the Momentum: Both experts agree that the AI trend is the dominant force in the market right now. Whether you follow Jones or Lee, being completely out of the market means missing a historic wealth-creation event.

- Monitor the Macro: Paul Tudor Jones reminds us that the “macro” environment matters. Keep an eye on the US fiscal situation and the “Over-equitization” levels he mentions. High valuations don’t cause crashes, but they do make markets more vulnerable to shocks.

- Focus on Quality: Follow Tom Lee’s lead by looking at earnings. As long as the semiconductor and tech leaders continue to beat earnings expectations and provide strong guidance, the bull market has a fundamental foundation to stand on.

- Have an Exit Strategy: Perhaps the most important takeaway from Jones is his concept of “Happy Feet”—staying nimble and having a plan to protect your capital if the technical trend breaks.

Conclusion

The debate between Paul Tudor Jones and Tom Lee highlights the complexity of the 2026 market. We are in a period of unprecedented technological change, but we are also carrying unprecedented levels of debt. By balancing the optimism of the AI revolution with the pragmatism of historical cycles, you can build a smart path to retirement that survives whatever comes next.

What is your take? Are we in 1999, or is this a brand-new era of growth? Let us know in the comments below.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always consult with a professional financial advisor before making investment decisions.