As an Amazon Associate, I earn from qualifying purchases.

In the world of investing, there is a common, often obsessive, focus on the “buy.” We spend countless hours researching the next big ticker, analyzing earnings reports, and scouring forums for the next “moonshot.” We treat the buying process as the honeymoon phase of our financial journey.

However, as many seasoned investors eventually realize, the buy is merely the beginning. The sell is where the real work happens. It is the decision to sell that determines whether you walk away with a profit, mitigate a loss, or keep your retirement timeline on track.

If you are planning for a specific milestone—like retiring at 67—you cannot afford to view selling as an afterthought. It is a critical, disciplined skill. In this post, we will explore why mastering the “exit strategy” is the most important part of your investment toolkit.

1. The Trap of the “Buy and Hold” Fallacy

“Buy and hold” is a classic strategy that has made many people wealthy. However, it is often misinterpreted as “buy and forget.”

The market is dynamic. Industries shift, business models get disrupted, and your personal financial needs change as you get closer to retirement. If you buy a stock simply because it was a good company ten years ago, but the fundamentals have eroded, holding onto it isn’t an investment strategy—it is a hope-based strategy.

The Golden Rule: Never confuse a company’s past performance with its future potential.

2. Your Investment Thesis is the North Star

Every time you buy a stock, you should have a clear, written reason for doing so. Did you buy it for its dividend growth? Its market dominance in tech? Or perhaps its undervalued assets?

This is your Investment Thesis.

The moment that thesis is invalidated, the reason for owning the stock is gone. For example, if you bought a retail stock because of its massive brick-and-mortar footprint, but e-commerce has rendered that footprint a liability rather than an asset, your thesis has been compromised. Selling is not an emotional decision here; it is a logical response to a changing reality.

3. The Power of Portfolio Rebalancing

For those of us working toward a 67-year-old retirement goal, portfolio rebalancing is our best friend.

Let’s say you have an allocation goal: 60% stocks and 40% bonds. If the stock market rallies significantly, your stocks might grow to represent 75% of your portfolio. Suddenly, your risk profile is completely different than what you intended.

This is the perfect time to sell. By trimming your stock positions to bring them back to 60%, you are effectively practicing “sell high.” You take those profits and reinvest them into the assets that have underperformed or are safer. This forces you to be disciplined, ensuring that a market crash doesn’t devastate your retirement fund.

4. Understanding Opportunity Cost

Every dollar tied up in a stagnating stock is a dollar that isn’t working for you elsewhere. This is the concept of Opportunity Cost.

Ask yourself this critical question: “If I had this money in cash today, would I buy this stock again at its current price?”

If the answer is no, why are you still holding it? Investors often fall into the trap of “loss aversion”—we hate to admit we were wrong, so we hold onto losing stocks hoping they will return to our purchase price. This is money that could be better deployed into a growing sector, a high-yield index fund, or even kept as cash to prepare for future market corrections.

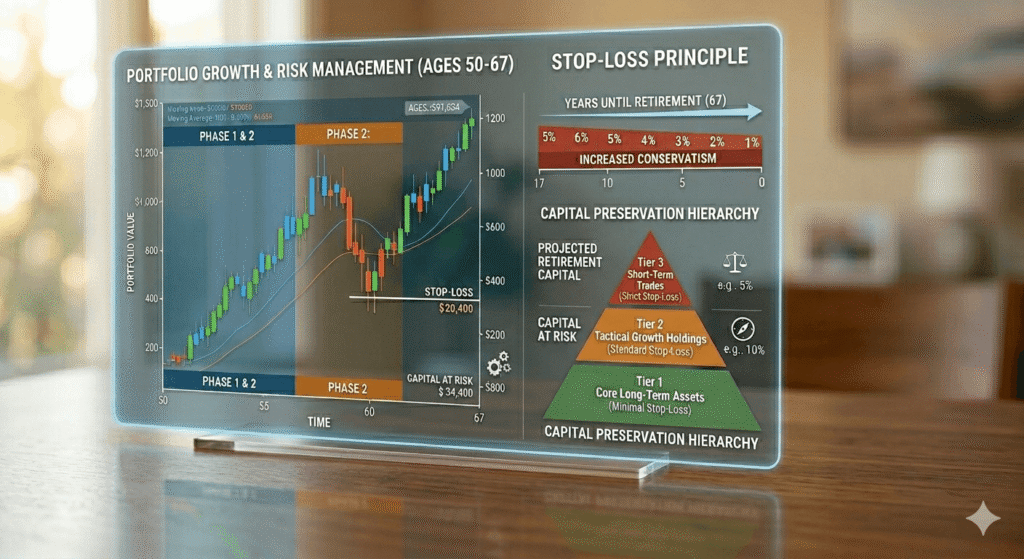

5. Setting “Hard Rules” to Protect Your Capital

As we age and edge closer to our target retirement date, the importance of capital preservation increases. We have less time to “wait out” a market correction than a 25-year-old investor.

To manage this, you should establish “hard rules” for exiting:

- The Percentage Stop-Loss: If a stock drops 10% or 15% from your purchase price, sell it automatically. This prevents a bad trade from becoming a portfolio-destroying disaster.

- The Valuation Ceiling: If a stock reaches a P/E ratio that is historically unsustainable, sell a portion of your position to lock in gains.

- The Time Limit: If a stock has been dead money for two years with no catalyst in sight, consider moving on.

6. The Psychology of Selling: Overcoming Fear and Greed

Selling is difficult because it triggers our deepest psychological biases.

- Greed: “What if it goes even higher?”

- Fear: “What if I sell and it immediately rebounds?”

To overcome this, use Incremental Selling. You don’t have to sell your entire position at once. If a stock hits your target price, sell 25% or 50%. This way, you lock in some profit (reducing your risk) while keeping some “skin in the game” if the stock continues to climb. This strategy helps manage the psychological toll of making big decisions.

Conclusion: The Path to Retirement

At Smart Path to Retire, we talk a lot about the journey to 67. Investing is the engine that drives that journey, but selling is the steering wheel. Without it, you are just along for the ride, hoping you don’t crash.

Don’t be afraid to pull the trigger. Whether it is to rebalance your portfolio, cut your losses, or realize a profit to fund your retirement lifestyle, selling is an act of stewardship. Treat your portfolio with the same care and professionalism you apply to your business operations.

Key Takeaways for Your Portfolio:

- Revisit your investment thesis quarterly.

- Don’t let emotions dictate your exit.

- Use partial sales to manage risk.

- Prioritize capital preservation as your retirement date nears.

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Always consult with a qualified financial advisor before making major investment decisions.