As an Amazon Associate, I earn from qualifying purchases.

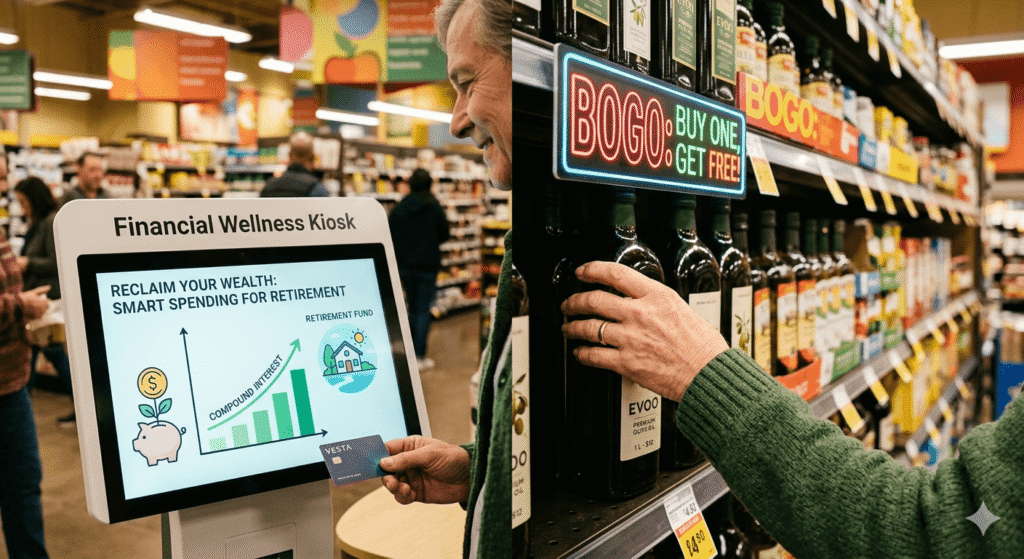

Every time you step into a grocery store, supermarket, or retail mall, you are greeted by giant, colorful signs shouting aggressive promises. “Buy One Get One Free!” (BOGO) or “Get One 50% Off!” flash before your eyes. These deals feel like a massive financial victory. In our minds, we instantly calculate a 50% discount and feel like smart, savvy shoppers beating the system.

But have you ever paused mid-aisle and asked yourself: Are these psychological sales signs actually saving me money? Or are they silently trapping my hard-earned cash and shrinking my retirement investment potential?

The truth is profound and highly critical for anyone preparing for retirement. For the average consumer, these promotions are rarely about real savings. Instead, they act as a “spending trap” designed to disrupt your personal cash flow, lock up your liquid capital, and steal away valuable compound interest opportunities.

1. The Real Anatomy of BOGO Marketing Tactics

To outsmart retail marketing, we must first understand the psychological architecture behind it. Grocery chains and big-box retailers do not design promotions out of generosity. They build them using advanced behavioral economics to optimize corporate profit margins.

The “Forced Budget Expansion” Trick

The primary illusion of a “Buy One, Get One Free” deal is that it represents an immediate 50% discount. However, the fundamental mechanism is entirely different. Instead of cutting prices, the retailer is actively forcing you to increase your transaction volume.

Imagine you walked into the store intending to purchase exactly one bottle of premium olive oil for $10. You see a “Buy One Get One 50% Off” sign. Suddenly, you find yourself spending $15 to acquire two bottles. From the store’s perspective, they successfully manipulated you into increasing your planned spending by 50%. You did not save $5; you spent an extra $5 that you had no intention of parting with when you walked through the sliding doors.

Dead Capital and Lost Opportunity Costs

When you purchase items you do not immediately need simply because they are on sale, that surplus money transforms into Dead Capital. This money sits quietly on your pantry shelves or deep inside your storage closets, completely locked down.

For someone actively preparing for retirement, every single dollar of liquid cash possesses a vital future utility value. When your cash is frozen inside an excess 24-pack of paper towels or duplicate jars of pasta sauce, that cash cannot earn a financial return. It is trapped money earning exactly 0% interest while gradually approaching an expiration date.

“Retail promotions don’t just consume your current income. They steal the future compounding power of that income.”

2. The True Math: BOGO vs. Consistent Market Investing

Let us look at the cold, hard numbers. Suppose these constant grocery store traps and retail temptations trick you into spending just an extra $50 every month. It seems completely harmless—just an extra $12.50 per week on item duplicates or bulk upgrades.

What happens if you break free from this consumer trap, discipline your shopping list, and redirect that exact $50 per month directly into a low-cost, broad-market index ETF (like an S&P 500 or Nasdaq-100 tracker) inside an investment account?

| Investment Timeline | Total Principal Contributed | Future Value (7% Annual Return) | Future Value (9% Annual Return) |

|---|---|---|---|

| 10 Years | $6,000 | $8,200 | $9,150 |

| 20 Years | $12,000 | $24,600 | $30,500 |

| 30 Years | $18,000 | $58,500 | $82,200 |

Look closely at those long-term projections. Over a standard retirement planning window, that seemingly invisible $50 a month transforms into $30,000 to over $80,000 in liquid wealth. By avoiding deceptive bulk sales and prioritizing investment consistency, you turn disposable retail clutter into substantial, real-world financial security.

3. The Hidden Traps: Perishability and Sunk Space

The financial damage of reckless BOGO shopping goes far deeper than just uninvested capital. It introduces two hidden secondary costs that quietly erode household efficiency: product expiration and structural space inflation.

- The Perishability Penalty: Food products carry hard, unforgiving expiration dates. If you buy a BOGO deal on yogurt, fresh produce, or meats and fail to consume the secondary item before it spoils, your discount drops instantly to 0%. In fact, you suffer a 100% net loss on the premium paid for the transaction. You paid a premium to throw garbage away.

- The Square Footage Tax: Storing excessive bulk items requires valuable physical space. When your home closets, cabinets, and garage shelves are packed tight with duplicate household cleaners or bulk dry goods, you are sacrificing living space to play warehouse manager for retail brands.

4. Actionable Rules for Smart Spending During Retirement Preparation

Transitioning into a successful retirement does not mean living in total deprivation. It means taking absolute ownership of your cash flow. Here is a practical blueprint to outmaneuver modern retail psychological traps:

Rule #1: Always Calculate the Absolute Unit Price

Never let bold storefront marketing banners do the math for you. Look closely at the small text on the store shelf tag to find the explicit price per ounce, per gram, or per individual sheet. Frequently, standard standalone items or different brands offer a vastly superior baseline unit price compared to hyped-up, bundle-deal packages.

Rule #2: The “Pre-Existing Intent” Litmus Test

Before dropping any promotional bundle or BOGO item into your shopping cart, stop and ask yourself one strict qualifying question:

“If this item was selling at its full, regular retail price today with zero signs around it, would it still be on my written shopping list?”

If the honest answer is no, you must put the item back on the shelf immediately. Buying an item solely because it is on sale is the definition of impulsive lifestyle inflation.

- Pro-Tip for Wealth Building: When you successfully resist a $15 BOGO temptation at the store, open your mobile banking app right there in the aisle. Instantly transfer that saved $15 directly into your retirement investment account. Moving saved money to your brokerage account turns psychological victories into physical, compounding assets.

Rule #3: Restrict Bulk Buying Exclusively to Non-Perishable Staples

Bulk purchasing and bundle discounts are only financially valid under very specific, controlled conditions. The items must be completely immune to rot or decay (such as high-quality toilet paper, laundry detergents, toothbrushes, or basic trash bags), you must possess a definitive, natural need for them within the upcoming quarter, and the purchase must fit comfortably within your current month’s fixed cash budget.

Conclusion: Reclaim Mastery Over Your Retirement Wealth

The popular saying goes, “A penny saved is a penny earned.” In the modern economy, however, a dollar shielded from clever marketing traps and safely deposited into a compounding investment account is worth vastly more than a closet filled with unwanted, expiring clutter.

True financial freedom in retirement is built on intentionality. By training your mind to see BOGO and bundle promotions as strategic corporate cash-grabs rather than consumer gifts, you protect your liquid capital. Take back control of your wallet, step away from the retail traps, and fuel your retirement portfolio instead.

Disclaimer: I am not a licensed financial advisor, broker, or tax professional. The content on this blog is for informational and educational purposes only and reflects my personal journey and research. Please consult with a qualified professional before making any financial decisions.