As an Amazon Associate, I earn from qualifying purchases.

RIn my ten years of running a small business, I’ve learned a hard truth: Revenue is vanity, profit is sanity. I have seen businesses with millions in sales go bankrupt because they couldn’t control their overhead. Conversely, I’ve seen lean operations thrive because they mastered the art of efficiency.

It took me longer than I’d like to admit to realize that the exact same rule applies to our personal finances.

We are culturally obsessed with the “Income Number.” We think, “If I only made $20,000 more a year, all my problems would disappear.” But as a 50-year-old in the “sandwich generation”—managing a team of seven, paying for college, and looking toward retirement—I’ve realized that the secret to wealth isn’t the size of your paycheck. It is the size of the gap between what you make and what you spend.

The “Income Illusion”

There is a dangerous trap called “Lifestyle Inflation.” As our income rises, our spending habits silently creep up to match it. That promotion? It just buys a more expensive car. That business bonus? It disappears into a renovated kitchen.

If you earn $100,000 but spend $99,000, you are functionally broke. If you earn $50,000 and spend $30,000, you are building wealth. It sounds simple, but in the noise of modern life, it is the hardest thing to execute. Being “wealthy” isn’t about the status symbols you possess; it’s about the financial freedom you’ve bought yourself by controlling your output.

Treating Your Life Like a Business

When I look at my business, I don’t just look at the top-line revenue. I look at expenses, margins, and reinvestment. Why don’t we do this with our personal lives?

To build wealth at 50, I had to stop viewing my spending as “what I can afford” and start viewing it as “what is necessary for my future freedom.” This required a radical shift in mindset:

- Stop Confusing “Affordability” with “Value”: Just because you can afford a $700 monthly car payment doesn’t mean you should have one. I ask myself: “Does this purchase provide long-term value, or is it just consuming my retirement capital?”

- Automate the Margin: In business, we know that if we wait until the end of the month to see what’s left over, there is usually nothing left. The same applies to personal finance. My wealth-building happens the moment my income hits my account. My savings are “paid” first, and I live on what remains.

- The Spending Audit: Every quarter, I look at my personal “P&L” (Profit and Loss). I track where the money goes. You would be shocked at how much “leakage” exists in small, recurring subscriptions and mindless spending that adds zero value to your happiness.

My “10% Rule” and the Power of Constraints

I’ve written before about my “10% Rule,” and it is the cornerstone of my spending philosophy. Constraints aren’t just for businesses; they are the best friend of the investor.

By setting a strict rule—such as investing 10% of my income automatically, or creating a “buy/sell” threshold for my portfolio—I take the emotion out of the decision. When you control your spending, you aren’t depriving yourself. You are merely reallocating resources from “present consumption” to “future security.”

Every dollar you don’t spend today is a dollar that earns interest for you while you sleep. That is the true secret of the wealthy: They make their money work for them, while the middle class works for their money.

Frequently Asked Questions (FAQ)

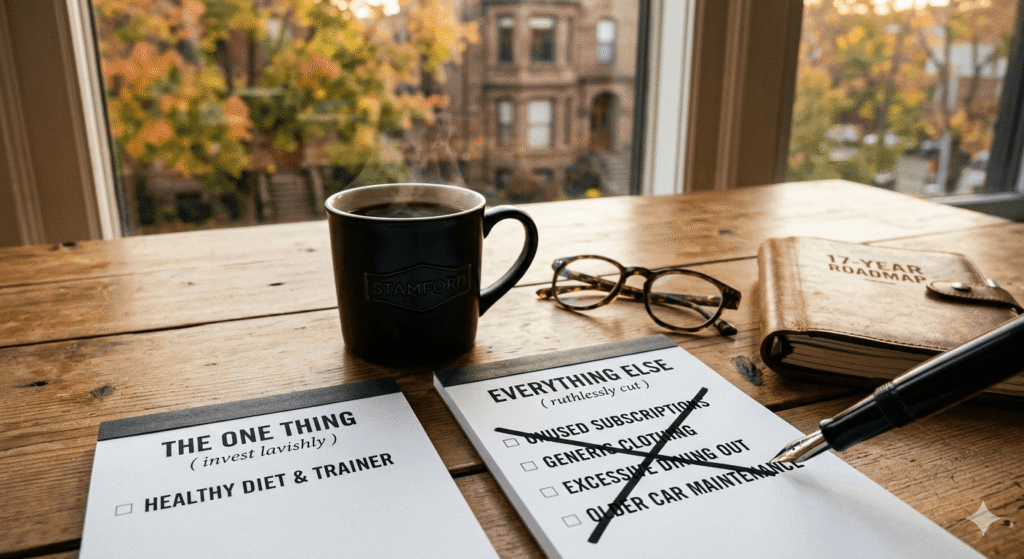

Q: Does this mean I can never enjoy my money? A: Absolutely not! The goal is not to live in poverty now to be rich later. The goal is to spend intentionally. Spend lavishly on the things that bring you joy and cut ruthlessly on the things that don’t. It’s about value, not austerity.

Q: What if my expenses are legitimately high (like college tuition)? A: This is the reality of the sandwich generation. If your expenses are high, you have to be even more creative with your income or be disciplined with your “discretionary” spending. It’s a season of life, but it doesn’t excuse us from planning.

Q: Is it too late to change my spending habits at 50? A: Not at all. 50 is a powerful time. You have the wisdom to know what truly matters. Changing a spending habit today has a compound effect for the next 17 years. It’s never too late to stop the leaks.

The Bottom Line

If you are waiting for a salary increase to start “getting wealthy,” you might be waiting forever. Wealth isn’t a salary level; it’s a habit. It is the practice of spending less than you earn and investing the difference with discipline.

Next time you are about to make a significant purchase, take a breath. Ask yourself: “Is this consumption moving me closer to my goal of retirement at 67, or is it pushing that date further away?”

Your future self is depending on the choices you make today. Let’s choose wisely.

Disclaimer: I am not a licensed financial advisor, broker, or tax professional. The content on this blog is for informational and educational purposes only and reflects my personal journey and research. Please consult with a qualified professional before making any financial decisions.