As an Amazon Associate, I earn from qualifying purchases.

Many people believe that the first step to retirement planning is investing.

But after entering my 50s and seriously thinking about retirement, I realized something different:

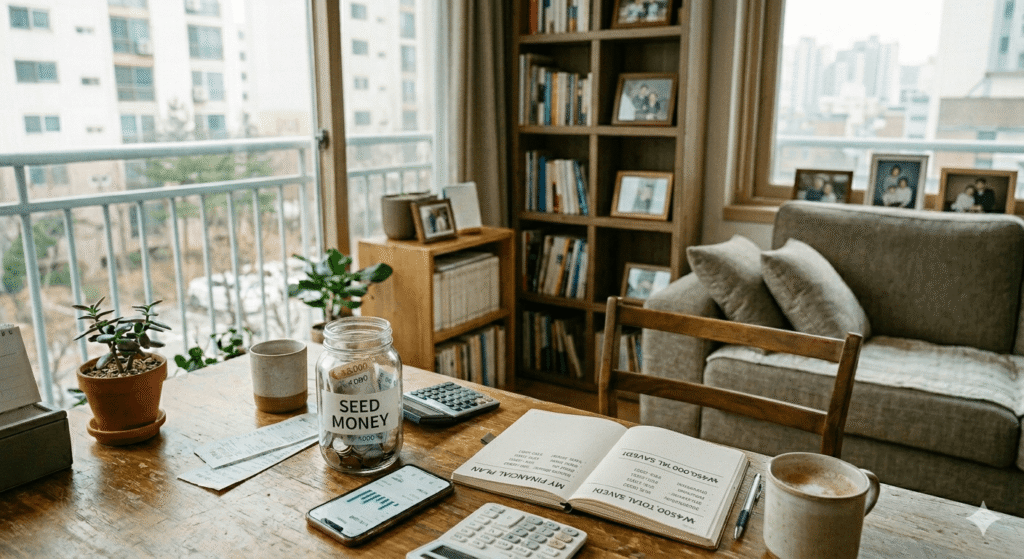

👉 You don’t start with investing. You start with creating seed money.

And surprisingly, that seed money doesn’t come from big changes.

It comes from small, everyday expenses that quietly drain your finances.

Why Small Expenses Matter More Than You Think

Let’s be honest—most of us don’t overspend on luxury items every day.

Instead, money disappears through:

- Daily coffee

- Impulse online purchases

- Frequent dining out

Individually, they seem small.

But over time, they add up to thousands of dollars.

👉 The key is not extreme frugality.

👉 The key is restructuring your spending habits.

1. The $5 Coffee Habit That Costs You $1,800 a Year

A daily $5 coffee doesn’t feel like a big deal.

But here’s the reality:

- $5 per day

- $150 per month

- $1,800 per year

That’s not pocket change—that’s potential investment capital.

Instead of cutting coffee completely, I made a simple shift:

👉 I started making coffee at home.

I didn’t go for anything complicated. A simple machine was enough to get started.

At first, I thought it would be inconvenient.

But it turned out to be faster, cheaper, and more consistent.

👉 The goal isn’t to eliminate enjoyment.

👉 It’s to change the system of spending.

2. The Hidden Problem: “Unnoticed Spending”

Most people don’t fail financially because of big purchases.

They fail because of:

👉 Small expenses they don’t track

Think about:

- Random Amazon purchases

- Small subscriptions

- “It’s cheap anyway” spending

So I started doing one simple thing:

👉 Writing everything down

Not an app. Not automation.

Just a physical planner.

And here’s what shocked me:

👉 “I didn’t realize I was spending this much.”

That awareness alone reduced my spending significantly.

3. Dining Out: The Silent Budget Killer

You don’t need to stop eating out completely.

But frequency matters.

When I reduced dining out:

- I spent less money

- I gained more control over my routine

- I avoided unnecessary add-on spending (delivery, tips, extras)

Instead of eating out 5 times a week, I cut it down to 2–3 times.

👉 The result?

A noticeable increase in leftover cash each month.

4. This Is Not About Saving—It’s About Reallocation

Most people hate budgeting because they think it means restriction.

But in reality:

👉 It’s not about spending less

👉 It’s about spending differently

For example:

- Coffee → Investment account

- Impulse buying → Index funds

- Dining out → Dividend stocks

When you see where the money goes,

👉 saving becomes strategy—not sacrifice.

5. What Happens When You Save Just $200 a Month?

Let’s keep it simple:

- $200/month

- $2,400/year

- $12,000 in 5 years (without investment growth)

Now imagine investing that consistently.

👉 That’s how real retirement preparation begins.

Not with a large lump sum,

but with consistent, intentional behavior.

6. Why This Approach Works for Beginners

If you’re in your 40s or 50s, this method is powerful because:

- It doesn’t require high income

- It doesn’t require financial expertise

- It builds discipline before investing

👉 And most importantly,

it creates confidence.

Conclusion: Retirement Starts with Control, Not Income

A lot of people think:

“I’ll start investing when I have more money.”

But the truth is:

👉 You need control before you need capital.

I didn’t start with a big financial plan.

I started with three simple changes:

- Coffee

- Tracking

- Dining out

And that alone created the space to invest.

✔ Final Takeaway

👉 Retirement planning doesn’t begin with investing. It begins with building your seed money.

🔧 My Simple Money Toolkit

These are the only tools I used to start reducing expenses and building investment capital:

👉 Simple tools—but powerful enough to change your financial habits.

💬 Final Note

This article contains tools that I personally use or carefully selected to help reduce unnecessary spending.

Feel free to explore them if you’re looking to take the first step toward building your investment seed money.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always consult with a professional before making investment decisions. This post contains affiliate links; we may earn a commission at no extra cost to you.