As an Amazon Associate, I earn from qualifying purchases.

We spend decades working, saving, and investing to build a retirement nest egg. As business owners, we obsess over quarterly earnings, operational efficiency, and market expansion. We treat our business as our primary engine for growth. But as we edge closer to the age of 67, there is one “silent killer” of retirement wealth that many investors overlook until it is too late: Taxes.

In the accumulation phase of your life, you are focused on growth. In the preservation phase—which you are currently entering—your mindset must shift. You are no longer just an investor; you are a tax manager. Every dollar you withdraw is a potential tax event. If you want to ensure your money lasts through your retirement years without diminishing your lifestyle, you need a strategy that prioritizes tax efficiency. Here is how you can keep more of what you have earned.

1. Understand Your “Tax Buckets”

Before you make a single withdrawal, you must understand where your money lives. Generally, your retirement assets fall into three distinct buckets, each taxed differently by the IRS. Mastering the order in which you tap these buckets is the foundation of tax efficiency.

- The Tax-Deferred Bucket (Traditional 401k/IRA): You didn’t pay taxes when you put the money in, so you pay taxes at your ordinary income rate when you take it out. This bucket is excellent for building wealth but can be a trap in retirement because it forces taxable income upon you.

- The Tax-Free Bucket (Roth IRA/401k): You paid taxes on the seed money, so the harvest—and all the growth—is entirely tax-free. This is your “freedom bucket.”

- The Taxable Bucket (Brokerage Accounts): You have already paid taxes on your income, and you pay taxes on capital gains and dividends. However, these are often taxed at lower long-term capital gains rates compared to ordinary income.

The Strategy: The secret is withdrawal sequencing. Usually, it is mathematically optimal to drain your taxable accounts first, then your tax-deferred accounts, and save your tax-free Roth assets for last. This allows your tax-free bucket to compound for as long as possible.

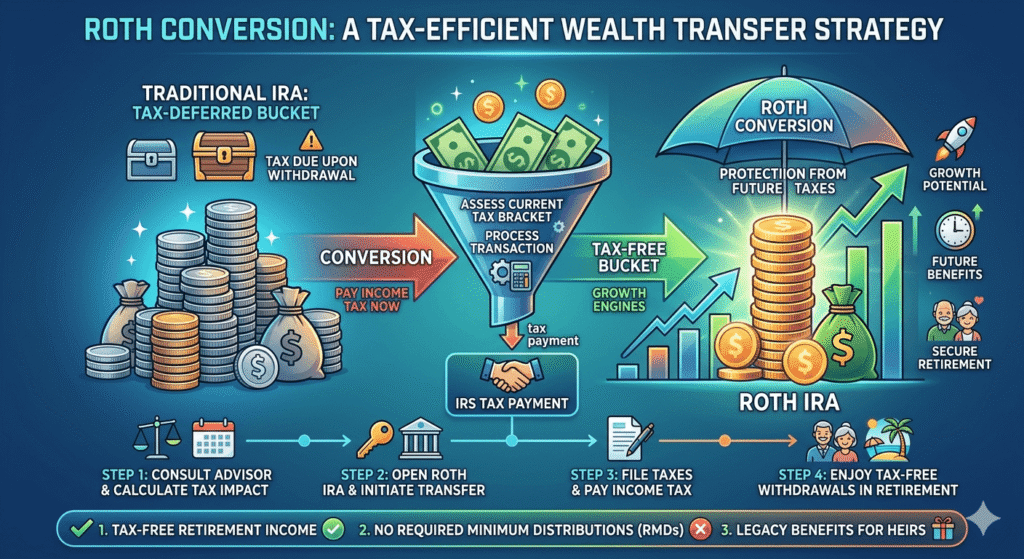

2. Strategic Roth Conversions: The Pre-Retirement Play

If you are in your 50s and still running a business, you might currently be in a higher tax bracket than you will be in early retirement (before Social Security and RMDs kick in). This “gap” creates a golden opportunity for Roth Conversions.

By converting a portion of your Traditional IRA to a Roth IRA, you pay taxes now at your current rate. Why would you do this? To prevent a massive “tax bomb” later. When you reach the age of Required Minimum Distributions (RMDs), the government forces you to withdraw from your Traditional IRA. If your account is too large, it could push you into a much higher tax bracket, effectively increasing your retirement tax bill. Strategic conversions smooth out your tax liability over time, ensuring you never hit a massive, unexpected tax spike.

3. The Power of “Asset Location“

Investors often confuse Asset Allocation with Asset Location. Allocation is about what you own (stocks vs. bonds). Location is about where you hold them.

You should be intentional about which accounts hold which assets. Generally, keep high-turnover, tax-inefficient assets (like bond funds or REITs that generate regular interest) in your tax-deferred accounts. Keep low-turnover, tax-efficient assets (like index ETFs or long-term growth stocks) in your taxable accounts. By being intentional about where you park your assets, you can minimize the “tax drag” on your returns, keeping more of your profits in your pocket instead of sending them to the IRS.

4. The Secret Weapon: The Health Savings Account (HSA)

Many people view the HSA merely as a way to pay for current medical bills. However, if you are a business owner or a high-earner, the HSA is actually a supercharged retirement vehicle.

It offers a triple tax advantage that no other account can match:

- Contributions are tax-deductible.

- Growth is tax-free.

- Withdrawals for qualified medical expenses are tax-free.

If you can afford to pay for your current medical expenses out of pocket and let your HSA grow invested in the market, it becomes a massive tax-free pool of capital that you can use for healthcare costs in your 70s and 80s. This is the ultimate hedge against rising healthcare costs in retirement.

5. Be Mindful of RMDs and Medicare Premiums (IRMAA)

The government wants its cut of your 401k eventually. Starting at age 73 (based on current laws), you must start withdrawing specific amounts every year via RMDs. Many retirees fail to plan for this and find themselves pushed into higher tax brackets, which triggers a secondary penalty: IRMAA (Income Related Monthly Adjustment Amount).

IRMAA is a surcharge on your Medicare Part B and Part D premiums based on your income. If your RMDs push your income too high, you could find yourself paying thousands of dollars extra in healthcare premiums. Start planning for your RMDs ten years in advance. If you know a big tax hit is coming, you can take steps now to mitigate it by drawing down your Traditional IRAs earlier or utilizing charitable giving strategies (Qualified Charitable Distributions).

Conclusion: Stewardship is the Final Stage of Investing

Retirement planning isn’t just about growth; it’s about control. By understanding how taxes impact your withdrawals, you move from being a passive saver to an active manager of your financial future.

You have spent years building your business and your wealth. Do not leave your financial legacy to chance—or to the tax authorities. Take the time to map out a tax-efficient withdrawal strategy today. It is the best way to ensure that the wealth you built stays with the people who matter most: you and your family. The path to 67 is paved with smart decisions—make tax management one of them.

Disclaimer: Tax laws are complex and subject to change. This post is for educational purposes only. Always consult with a tax professional or a certified financial planner before making major changes to your retirement strategy.