As an Amazon Associate, I earn from qualifying purchases.

As I look at my 17-year horizon toward retirement, I often compare my investment strategy to the business I have run for the past decade. In business, you don’t just rely on one product to sustain the company forever; you balance your stable, cash-flowing lines with innovative new ventures. You must protect the foundation, but you also need to identify the new trends that will drive future revenue.

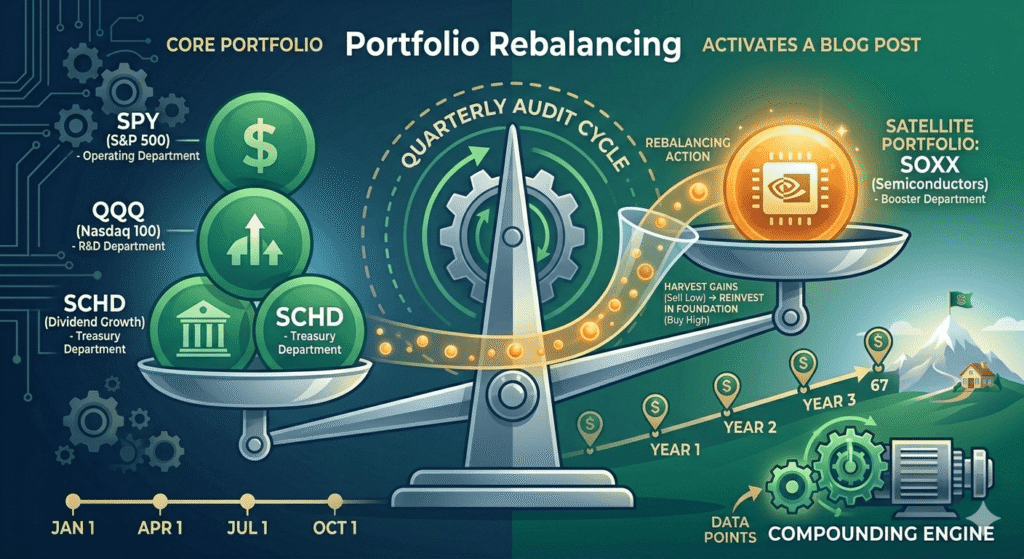

My retirement portfolio is built the same way. While I advocate for a “Core” strategy—using SPY (S&P 500), QQQ (Nasdaq 100), and SCHD (Dividend Growth)—I have learned that being too static is a mistake. To truly optimize for growth while managing risk, you need to incorporate a “Satellite” strategy, and more importantly, you need the discipline of rebalancing.

The Foundation: Your Core “Departments”

To understand why I keep a Core portfolio, we must look at the function of these ETFs. They are not just tickers on a screen; they are the departments of my financial business:

- SPY (S&P 500): This is the Operational Department. It provides the reliable, broad-market growth that keeps the business stable. It is the bedrock of the U.S. economy.

- QQQ (Nasdaq 100): This is the R&D Department. It is designed for innovation. By capturing the growth of the top non-financial companies, it injects the necessary velocity into my portfolio.

- SCHD (Dividend Growth): This is the Treasury Department. It focuses on companies with a history of sustainable payouts, providing the cash flow that helps dampen the effects of market volatility.

These three ETFs are the engines that will carry me to my $750,000 goal. They represent the “Core.” They are not meant to be traded daily; they are meant to be nurtured over decades.

The Satellite: Capturing Market Flow with SOXX

While my Core is stable, the world is moving fast. A business owner who ignores the market shifts dies. Today, we are witnessing a technological transformation driven by AI, cloud computing, and automation. At the heart of all this is one vital component: the semiconductor.

This is where the “Satellite” strategy comes in. I use SOXX (iShares Semiconductor ETF) as a targeted booster. Semiconductors are the infrastructure of the future. By allocating a smaller percentage (the Satellite) of my portfolio to SOXX, I gain exposure to the companies designing the chips that power the modern world—companies like NVIDIA, Broadcom, and Qualcomm.

The key here is allocation, not obsession. My Core holds the bulk of my capital, while SOXX represents a strategic tilt toward a sector I believe has long-term structural tailwinds. I don’t buy SOXX to “get rich quick”; I buy it because I want my portfolio to capture the current and future flow of the global economy.

The Secret Ingredient: Rebalancing (The Quarterly Audit)

Here is where many retail investors fail. They buy, they watch, and they never touch their portfolio again. But if you were running a business, would you allow your R&D budget to swell to 80% of your total expenses because of a sudden boom, while neglecting your core operations? Of course not.

Rebalancing is the quarterly audit of your portfolio.

If I set my target allocation at 80% Core (SPY/QQQ/SCHD) and 20% Satellite (SOXX), what happens when SOXX surges by 40%? Suddenly, my Satellite component might balloon to 28% of my total portfolio.

Does this mean I should “let it ride”? No. As a disciplined investor, I see this as an imbalance. I have become over-exposed to the volatility of a single sector. This is the moment to rebalance:

- Sell High: I harvest the gains from my SOXX position, effectively “locking in” the profits that the market gave me.

- Buy Low: I move those profits into my Core holdings (SPY, QQQ, SCHD). This lowers my average cost basis in these core assets, effectively buying more shares of the foundation while they are potentially under-weighted.

- Reset: My portfolio is now back to its intended 80/20 risk profile.

This process is profoundly counter-intuitive to most people. It forces you to sell your “winners” and buy your “under-performers.” But it is the only way to ensure that your risk tolerance remains consistent over 17 years. Rebalancing prevents you from becoming “accidentally” exposed to more risk than you can handle.

Avoiding the Trap of “Market Timing”

Many readers ask, “Can’t I just time the market? Buy when SOXX is low, sell when it’s high?”

The answer is: no. Market timing is a game for traders. As an entrepreneur, I don’t have the time or the desire to stare at charts all day. My strategy relies on systematic rebalancing. Whether the market is up or down, I check my portfolio every quarter. If it’s out of alignment, I fix it. This removes the emotion from the decision. I am not predicting the market; I am simply keeping my asset allocation in line with my long-term financial goals.

The Business Owner’s Mindset

Investing, at its core, is just another form of capital allocation. If you treat your portfolio like a business—with a clearly defined core strategy, intentional satellite bets, and rigorous quarterly audits (rebalancing)—you significantly increase your probability of success.

We aren’t here to gamble on the next “hot” stock. We are here to build an engine that works. We want the Core to provide the steady hum of growth, the Satellite to provide the spark of innovation, and our Rebalancing discipline to ensure that we never lose our way.

Your Call to Action

I encourage you to look at your own portfolio today. Are you simply letting it grow, or are you actively managing it? If you haven’t reviewed your asset allocation in the last six months, your portfolio has likely drifted from its intended risk level.

- Check your current allocations. Is one sector dominating your account?

- Set a rebalancing schedule. Decide whether you will rebalance annually or quarterly.

- Don’t wait for a market correction. Fix your allocation while the sun is shining, not when you are panicking during a storm.

Investing is a journey, and like any journey, you need to check your map and adjust your course regularly. Let’s keep building our “Smart Path to Retire.”

Disclaimer: I am not a licensed financial advisor, broker, or tax professional. The content on this blog is for informational and educational purposes only and reflects my personal journey and research. Please consult with a qualified professional before making any financial decisions.