As an Amazon Associate, I earn from qualifying purchases.

When I first started my investment journey, I had a clear vision: I would be the genius who found the next “ten-bagger”—a stock that would return 10 times my initial investment. I spent hours reading forums, chasing “hot” micro-cap stocks, and listening to influencers who promised that the next big thing was just around the corner.

I was convinced that my business acumen would help me spot diamonds in the rough that Wall Street had missed.

I was wrong.

Today, after years of trial and error, I want to share a hard-earned truth with those just starting out. The dream of the “ten-bagger” is seductive, but for a beginner, it is often a trap. If you want to build a real retirement, you need to look at what actually drives the market: the giants.

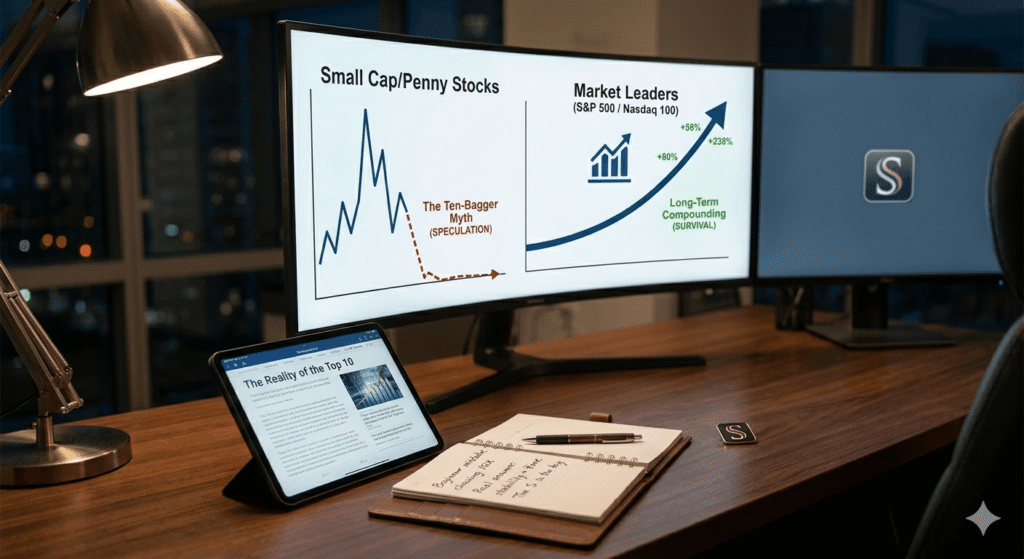

The Trap: Why Small-Caps Break Your Heart

In the beginning, I loved the idea of small-cap stocks. When the economy is booming, small companies can indeed deliver explosive returns. They are agile, and a little bit of growth looks massive in terms of percentage.

But there is a catch. When the market turns—and it always turns—small-cap stocks don’t just “dip”; they crater. They lack the capital reserves, the brand loyalty, and the operational infrastructure to weather a storm.

I remember watching my “hidden gems” drop 30%, 40%, 50% in a single month. I kept telling myself, “It will bounce back.” But it didn’t. Many of those companies didn’t just fail to bounce back; they effectively went to zero. As a business owner, I know that survival is the first rule of success. If your business model is fragile, the market will eventually find that weakness. Most small-cap “winners” are simply too fragile to survive a genuine economic downturn.

The Reality: The “Top 10” Rule

While I was losing sleep over volatile small-caps, I started looking at the broad market data. I noticed something undeniable: The S&P 500 is not a democratic index. It is heavily skewed toward the top 10 companies.

Companies like Apple, Microsoft, Nvidia, Amazon, and Google are not just “stocks”; they are the infrastructure of modern civilization.

- Cash Flow: These companies have cash piles larger than the GDP of many countries.

- Moats: They possess “economic moats”—barriers to entry—that make it nearly impossible for competitors to displace them.

- Resilience: When the economy slows down, these companies have the resources to innovate, acquire competitors, and survive until the next upcycle.

I realized that while my small-cap stocks were struggling to keep the lights on during a downturn, the Big Tech giants were simply “taking a breath.” Within a few quarters, they were not only back to their previous highs but were hitting new records. They aren’t just market leaders; they are the market.

Why Beginners Should Start with the Giants

If you are a beginner, you don’t need a “ten-bagger” to retire. You need compounding.

The mistake I made early on was viewing investing as a lottery ticket. Investing is not about winning one big game; it is about staying in the game for decades. Big Tech and market leaders offer three things that every beginner needs:

- Visibility: You use their products every day. You don’t have to guess if their business model works; you know it works because you are a customer.

- Lower Volatility: They still swing, but they don’t break. You can sleep at night knowing your investment isn’t going to vanish because of a bad quarterly earnings report.

- Growth Trajectory: Look at the chart of any major tech leader over the last 20 years. It’s a stair-step to the right. That is what you want for your retirement fund.

How to Apply This (Without Overcomplicating It)

I don’t want you to abandon the stock market because of the “ten-bagger” myth. I want you to change your strategy to one that actually works.

- Own the Index: Instead of trying to guess which specific tech company will win, buy the S&P 500 (SPY) or the Nasdaq 100 (QQQ). By doing this, you automatically own the winners. When a small company grows into a giant, the index eventually adds it. When a giant fails, the index removes it.

- Prioritize Stability over Excitement: Investing should be boring. If you are getting a dopamine rush from checking your stock app every 10 minutes, you aren’t investing—you’re gambling.

- Focus on Your “Core”: Treat your portfolio like your own business. Put your capital into “profitable,” “proven,” and “durable” assets.

Final Thoughts: Be a Rational Investor

The journey to $750,000—or whatever your retirement number is—isn’t a sprint. It’s a marathon. You don’t need to hit a home run every time you step up to the plate. You just need to keep hitting singles and doubles, and let time do the heavy lifting.

Don’t let the allure of quick riches keep you from building lasting wealth. Buy the leaders, trust the process, and give your money the time it needs to compound. You have a business to run and a life to enjoy—don’t spend your time chasing mirages.

Disclaimer

The information provided on Smart Path to Retire is for educational and informational purposes only and does not constitute professional financial, investment, or legal advice.

As a business owner sharing my personal journey toward retirement, the strategies and asset allocations discussed here reflect my own opinions, risk tolerance, and research. They are not intended to be—and should not be interpreted as—financial advice or a recommendation to buy or sell any specific securities.

- Investment Risk: All investing involves risk, including the possible loss of principal. Markets are volatile, and past performance is never a guarantee of future results.

- Do Your Own Research (DYOR): Every individual’s financial situation, goals, and risk tolerance are different. You should conduct your own due diligence and consult with a qualified financial advisor, tax professional, or accountant before making any investment decisions.

- No Guarantees: Any mention of specific returns, financial goals, or growth projections is purely illustrative and based on historical data or personal planning. No specific financial outcome is guaranteed.

By using this website, you acknowledge that you are responsible for your own financial decisions. The author of Smart Path to Retire shall not be held liable for any losses or damages resulting from the use of, or reliance on, the information provided on this site.