As an Amazon Associate, I earn from qualifying purchases.

The financial world was rocked this week as the U.S. Bureau of Labor Statistics released the April Consumer Price Index (CPI) report. The data revealed that inflation surged to 3.8% year-over-year, marking the highest level in nearly three years since the peak of the post-pandemic supply chain crisis.

For many investors, especially those meticulously planning for retirement, this wasn’t just a statistic—it was a wake-up call. The dream of a mid-year interest rate cut by the Federal Reserve has effectively evaporated, replaced by the grim reality of “Higher for Longer.” In this comprehensive guide, we will break down why inflation is rebounding and, more importantly, how you can protect your retirement nest egg from losing its purchasing power.

1. The Anatomy of the April CPI Shock: Why Now?

The 3.8% print caught many analysts off guard. While the market hoped for a cooling trend toward the Fed’s 2% target, several factors converged to push prices higher.

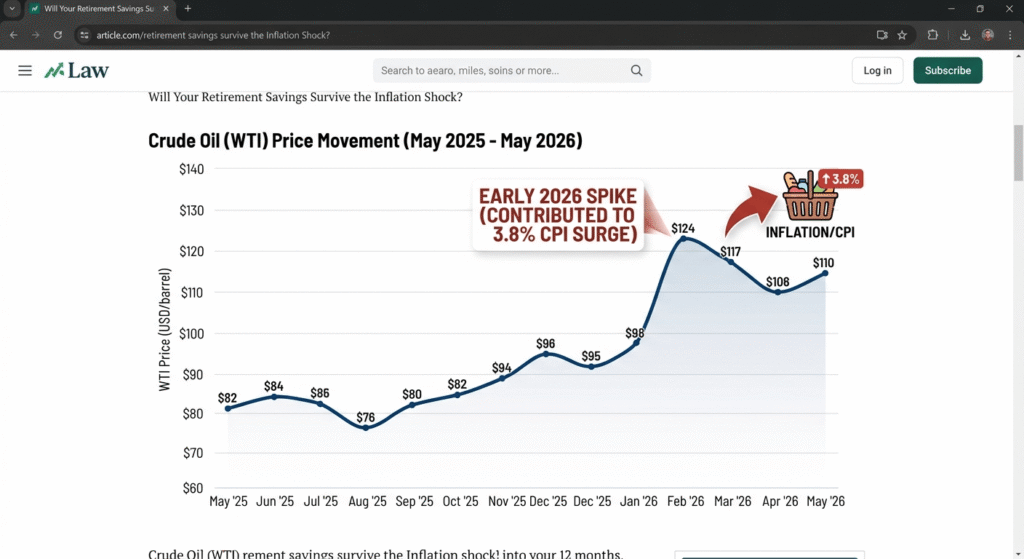

The Energy Crisis Re-ignited

The primary culprit behind the April surge was energy prices. Geopolitical tensions in the Middle East escalated significantly last month, pushing crude oil prices above the $120 per barrel mark. This spike didn’t stay at the pump; it filtered through the entire economy, increasing transportation costs for groceries, consumer goods, and industrial supplies.

Sticky Service Inflation

Beyond energy, “sticky” inflation in the service sector—including insurance, healthcare, and housing—remains stubbornly high. When service costs rise, they tend to stay up longer than commodity prices, making the Fed’s job of cooling the economy much more difficult.

2. The Fed’s Dilemma: The Death of the “Rate Cut” Narrative

For months, Wall Street has been betting on a series of interest rate cuts starting in the summer of 2026. The April CPI report has essentially demolished that timeline.

- Higher for Longer: Federal Reserve officials have hinted that without “clear and convincing” evidence of inflation heading to 2%, they cannot justify lowering rates.

- The Risk of a Hike: While a rate hike isn’t the baseline scenario yet, the conversation has shifted. If inflation remains near 4%, the Fed may have to keep the federal funds rate at its peak for the remainder of the year, or even consider a final “insurance” hike.

For retirees, this is a double-edged sword. While high rates offer better yields on savings accounts and CDs, they also create significant volatility in the stock market, particularly for growth-oriented tech stocks.

3. Is Your Retirement Portfolio Safe? Assessing the Impact

Inflation is often called the “silent thief” because it erodes the value of your money without you noticing. A 3.8% inflation rate means that $1,000,000 today will only have the purchasing power of roughly $962,000 in just one year.

The Tech Sector Vulnerability

If your retirement account is heavily weighted toward high-growth tech companies (like NVDA, AMZN, or AAPL), you might see increased volatility. These companies rely on future earnings, which are discounted more heavily when interest rates stay high.

The Bond Market Trap

Investors holding long-term bonds have seen their principal value drop as yields rise in response to inflation. If you are close to retirement, having too much exposure to long-term debt without inflation protection could be a risk.

4. Strategic Adjustments: How to Defensive-Proof Your Savings

In a 3.8% inflation environment, staying stagnant is a losing strategy. Here is how you should consider rebalancing your portfolio:

A. Focus on Cash Flow (Dividend Growth)

When capital gains become uncertain due to market volatility, dividends become your best friend. Look for companies with a history of increasing dividends even during economic downturns. Dividend Aristocrats or ETFs like SCHD (Schwab US Dividend Equity) provide a psychological and financial buffer. The income generated can be reinvested or used to cover rising living costs without selling your principal shares.

B. Embrace Inflation-Hedge Assets

Real assets tend to perform well when the dollar loses value.

- Gold: Traditionally a store of value during inflationary periods.

- Energy Stocks: Since energy is driving the CPI, owning the producers can act as a natural hedge.

- Commodities: Broad exposure to raw materials can protect against rising consumer prices.

C. Short-Term Fixed Income

With the Fed keeping rates high, short-term Treasury bills and high-yield savings accounts are finally offering meaningful returns (often 5% or higher). This allows you to earn a “real” return (yield minus inflation) with virtually zero risk to your principal.

5. The Psychological Game: Staying the Course

The most dangerous thing an investor can do during a “CPI Shock” is to panic-sell. Market cycles are inevitable. While 3.8% inflation is high compared to the last decade, it is far from the hyperinflationary periods of the late 1970s.

Remember your horizon. If you are 50 years old today, you are investing for a 30-year window, not a 3-month window. Use market dips as an opportunity to accumulate high-quality assets at a discount. Inflation eventually cools, and the companies that survive these periods often emerge with stronger pricing power and better margins.

Conclusion: Take Control of Your Financial Future

The April CPI report is a reminder that the path to economic stability is rarely a straight line. While the delay in interest rate cuts is frustrating, it provides a crucial moment for you to audit your retirement plan.

Ask yourself:

- Does my portfolio have enough exposure to inflation-resistant assets?

- Is my cash flow (dividends/interest) sufficient to cover rising costs?

- Am I diversified enough to handle a “Higher for Longer” interest rate environment?

Inflation may be at a 3-year high, but with a disciplined strategy and a focus on quality, your retirement goals can remain firmly on track.

Stay informed, stay invested, and stay disciplined.