As an Amazon Associate, I earn from qualifying purchases.

At 50 years old, the traditional narrative tells me that I should be preparing to slow down. I am told to protect my capital, reduce my risks, and watch the calendar until 67. But after running a company for the last decade, I don’t see age 50 as a “winding down” phase. I see the next 17 years as the most critical capital allocation phase of my professional life.

In business, you cannot succeed without a clear revenue target and an operating budget. If I ran my company by simply hoping for growth without allocating specific capital to marketing, operations, or research, I would have gone bankrupt years ago. Yet, when it comes to retirement, most people treat it like a savings project—something passive that they hope will grow on its own.

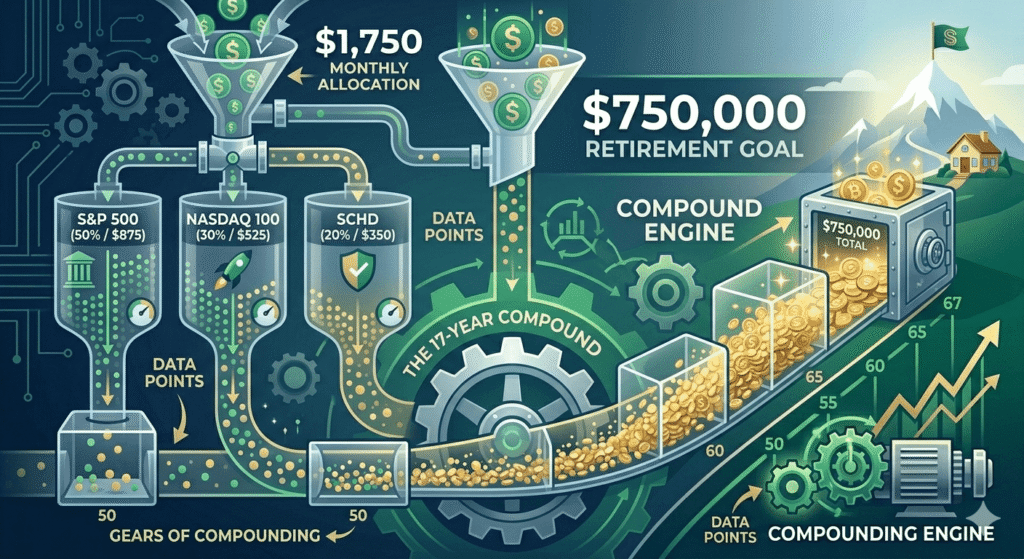

I am treating my retirement differently. I am treating it like a business unit. My target is $750,000 by age 67. To reach that, I am not just “saving”; I am executing a 17-year operational plan.

The Business of Retirement: Departmental Allocation

Just as I divide my business into operational sectors to ensure efficiency, I have divided my investment portfolio into three “departments.” Each ETF I hold serves a specific purpose in my balance sheet:

1. S&P 500: The ‘Operations and Management’ Department This is the core of my business. The S&P 500 represents the foundation of the U.S. economy. It provides the stability and consistent, underlying revenue growth necessary to keep the business—my portfolio—alive and well. It is not designed for flash; it is designed for scale and longevity. This department receives the largest portion of my capital because, without a strong base of operations, the entire structure is at risk.

2. Nasdaq 100: The ‘R&D’ Department A business that does not innovate is a business that dies. The Nasdaq 100 represents the R&D arm of my retirement plan. Yes, the R&D department is expensive, and yes, it comes with higher volatility. It requires a stronger stomach because the breakthroughs—and the losses—can be larger. But over a 17-year horizon, I need this exposure to technology and innovation to drive the growth that standard operations alone cannot provide.

3. SCHD: The ‘Treasury and Cash Flow’ Department In my company, I know that revenue is vanity, but cash flow is sanity. SCHD (the Schwab US Dividend Equity ETF) is my Treasury. It focuses on companies with a history of sustainable dividends and financial health. This department provides the cash flow—the dividends—that I can reinvest immediately. It acts as a stabilizer, ensuring that even in volatile years, the “business” is still generating tangible returns.

The $750,000 Operational Plan

A target of $750,000 over 17 years is an achievable objective if we treat it with the discipline of a monthly expense. Assuming a conservative but realistic average annual return of 8%, I need to supply this engine with a consistent stream of capital.

To reach $750,000 by age 67, I have calculated that I must commit to a monthly capital injection of $1,750.

This is not a “contribution”—this is an operating expense. It is as non-negotiable as the rent for my office or the payroll for my employees. To maintain the balance of my “departments,” I distribute this $1,750 as follows:

- S&P 500 (50% / $875): My foundational operating capital.

- Nasdaq 100 (30% / $525): My growth-oriented R&D investment.

- SCHD (20% / $350): My treasury department, focusing on sustainable dividends.

By automating this $1,750 transfer, I remove the human element. I don’t have to decide whether to invest during a market dip or a market peak. I simply supply the capital, and the engine does the work.

The Discipline of the CEO

The single greatest threat to this 17-year plan is not a market crash; it is the CEO—me—interfering with operations.

In my business, if I fired my best employees every time we had a bad quarter, my company would collapse. The same applies here. When the Nasdaq 100 dips, I don’t “fire” the R&D department. When the S&P 500 has a down month, I don’t cut the operations budget. I stay the course. The math of compound interest only functions when the timeline is uninterrupted.

Market volatility is the “operating cost” of achieving high returns. If you want the 8% growth, you must be willing to endure the fluctuations that come with it. By keeping my contributions consistent, I am essentially “buying the dip” automatically. When prices are high, my $1,750 buys fewer shares; when prices are low, my $1,750 buys more. This dollar-cost averaging is the hallmark of a disciplined manager.

The Final Harvest

We have spent decades building skills, creating value, and running businesses. We have played the role of the worker and the manager. Now, we are entering the final act: the role of the owner.

In 17 years, at age 67, I won’t be looking at my portfolio as a collection of tickers. I will be looking at it as a finished facility. I will have built a $750,000 asset that is capable of sustaining me.

There is no such thing as being “too late” to start, provided you are willing to build. Whether you are 50, 45, or 55, the math remains the same. You need a target, a set of operational departments (your ETFs), and the iron-clad discipline to supply them with capital every single month.

Is your retirement plan an active business strategy, or is it just a hope? If it’s the latter, change your approach today. Determine your number, set your contribution, and start your engine. You have 17 years. Let’s make them count.

Disclaimer: I am not a financial advisor. This is a personal strategy based on my specific business situation and risk tolerance. Every investor’s journey is unique, and you should adjust these allocations to fit your own financial goals. Please conduct your own research before making financial decisions.