As an Amazon Associate, I earn from qualifying purchases.

For the past three years, my focus has been on growth. I bought ETFs, I hand-picked stocks, and I watched the numbers tick upward. It’s been an exciting ride. But recently, I had a realization: A high portfolio balance doesn’t pay the electric bill. When I look at my retirement, I don’t just want a “big number” in a brokerage account. I want a steady, reliable stream of cash that hits my bank account every month, regardless of whether the stock market is having a good day or a bad one.

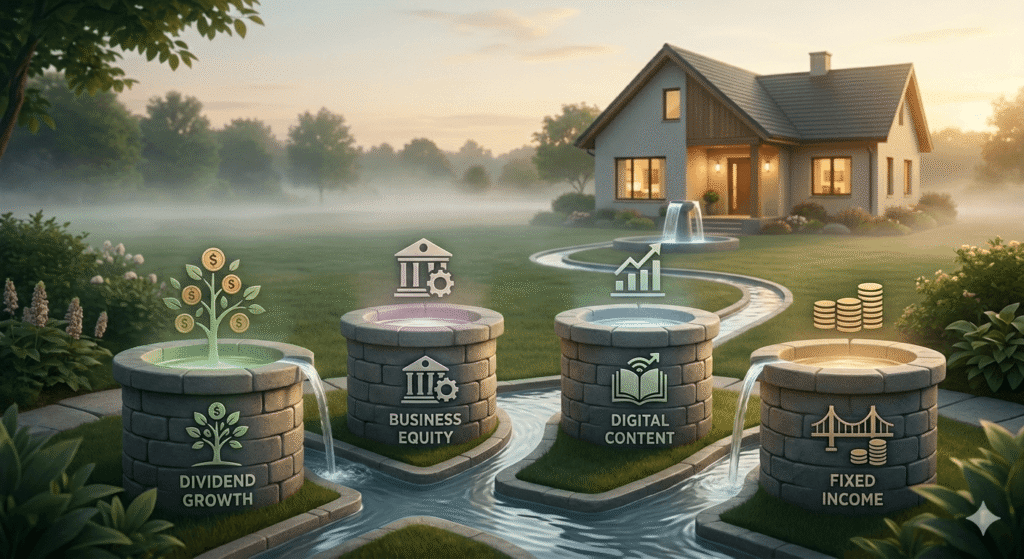

Experts often talk about “creating multiple wells” of income. If one well dries up (like a market crash affecting stock prices), the others keep the water flowing. As I look at my 10-asset portfolio—my 3 ETFs, 1 bond fund, and 6 stocks—I am actively transforming them into a system of income. Here is the “4-Well Strategy” I am using to prepare for age 67.

Well 1: The Dividend Growth Well (The “Market” Well)

My first well is the market itself, but I am viewing it differently now. I’m no longer just looking for the next “hot” stock; I am prioritizing assets that pay me to own them.

Within my 3-ETF allocation, I am focusing on funds that emphasize Dividend Growth. The beauty of dividend stocks isn’t just the yield today; it’s the fact that good companies increase their payouts every year. By the time I hit 67, these dividends will be significantly higher than they are today. This well provides the “passive” income that grows while I sleep, shielding me from the need to sell my principal shares when the market is down.

Well 2: The Business Owner’s Well (The “Active” Well)

As a business owner, this is my strongest asset. Many retirees treat their business as something to “close down” upon retirement. I view mine as an income-producing asset to be managed, sold, or structured for long-term profit.

Instead of waiting for a one-time “exit” payday, I am looking for ways to maximize the operational profit of my business. Can it run with less of my time? Can it be structured to provide a management fee or a recurring profit share even after I step back? My business isn’t just a job; it’s a capital-generating machine that feeds my investment portfolio today, and it will be a source of “consulting” or “ownership” income tomorrow.

Well 3: The Digital/Content Well (The “Scalable” Well)

This is where my retirement blog, Smart Path to Retire, comes in. In the digital age, content is an asset. When I write a post about retirement planning, I am creating something that can generate ad revenue (AdSense) or affiliate income for years.

Unlike a stock, which requires capital to buy, this well requires sweat equity. By building this blog now, I am creating a “Digital Real Estate” asset. By the time I am 67, this will be a fully established platform. Whether it’s through ad revenue, digital products, or community subscriptions, this well doesn’t rely on the S&P 500—it relies on the value I provide to my readers. That is an incredibly powerful, uncorrelated income stream.

Well 4: The Fixed Income Well (The “Stability” Well)

Finally, I have my 1 Bond Fund. This is the “safe” well. It’s not meant to make me rich; it’s meant to keep me solvent.

In retirement, you cannot afford to have 100% of your money in volatile assets. If a major market crash happens right when you retire (known as Sequence of Returns Risk), selling stocks at a loss is devastating. My bond fund is my buffer. It is the well I draw from when the other wells are temporarily low. It provides the liquidity I need to weather market storms without panic-selling my growth stocks.

The CEO Mindset: Optimal Risk Management

How do I protect these wells? I treat them like business departments.

- Rebalancing is my “Audit”: Every quarter, I check my 10 assets. If my growth stocks (my satellite assets) have skyrocketed, I trim them and “pour” the profits into my dividend-growth well or my fixed-income well. This automatically locks in gains.

- Diversification is my “Insurance”: By having four distinct types of income, I am not dependent on any single entity. If the market crashes, my business income remains. If my business has a slow quarter, my dividend income remains.

Why This Shift Matters Now

The mistake most investors make is waiting until they are 66 years and 364 days old to think about income. By then, it’s too late to build a new well.

At 50, I have 17 years. That is enough time to dig deep, build the infrastructure, and let the compounding effect take hold. I am not trying to “retire” from life; I am trying to “graduate” from the daily grind by having systems that pay me to exist.

Final Thoughts

Retirement isn’t an age; it’s a financial state. It’s the point where your “wells” generate more water than you need to drink. My 40% return over the last three years was a great start—it was the initial capital that allowed me to build the foundation. But from here on out, my job is to ensure those wells are deep, sustainable, and diversified.

How about you? You’ve likely built a great portfolio, but have you thought about which “wells” will provide your income in retirement? Are you relying solely on your stock portfolio, or are you looking into other streams like business equity or content?

I’d love to hear your thoughts in the comments below. Let’s help each other plan for a future that isn’t just wealthy, but secure.

Disclaimer: I am not a financial advisor. This is a personal strategy based on my specific situation and risk tolerance. Every investor’s journey is unique, and income strategies should be tailored to your own goals. Please consult with a professional before making major financial decisions.